Buying your first investment property in Wellington can feel complex, but it does not have to be stressful. With the right research, a clear financial plan, a data-driven mindset, and a strong professional team, first-time investors can enter the Wellington market with confidence. This guide explains how to assess suburbs, prepare financially, avoid emotional decision-making, and set up your investment for long-term success.

Table of Contents

Introduction

For many New Zealanders, purchasing a first investment property is both exciting and intimidating. Wellington, with its strong rental demand, diverse suburbs, and steady employment base, continues to attract new investors. At the same time, rising interest rates, changing regulations, and high property prices can make the process feel overwhelming.

If you are considering first property investment NZ, this guide is designed to cut through the noise. It focuses on practical steps, reliable data, and professional insights that help you make confident decisions when buying an investment property in Wellington.

The reality of first-time property investment

Your first rental property is different from buying a home to live in. Emotional attachment, lifestyle preferences, and personal taste matter far less than numbers, compliance, and tenant demand.

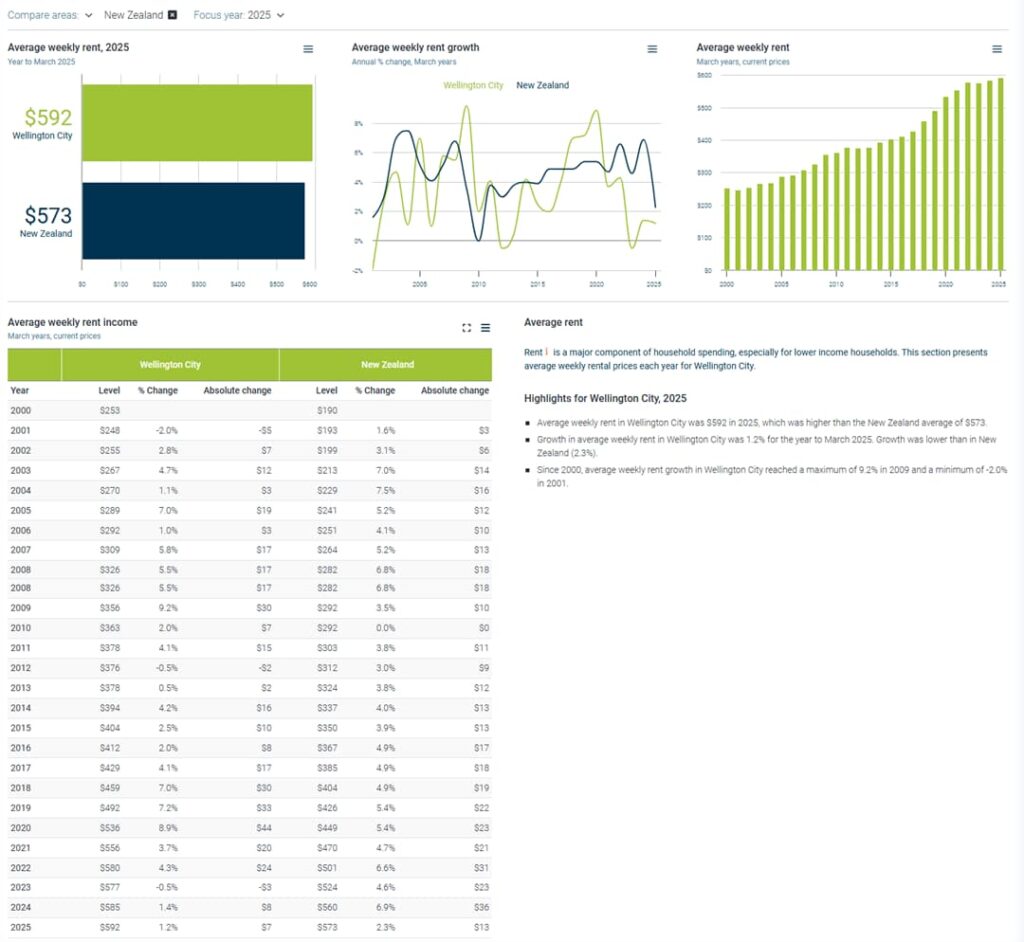

According to the REINZ (Real Estate Institute of New Zealand), Wellington remains one of the country’s strongest rental markets due to its concentration of government, education, healthcare, and professional services. These sectors provide a consistent tenant base even during economic slowdowns.

That consistency is reassuring for first-time investors, but success still depends on preparation and discipline.

Research and due diligence: Choosing the right Wellington suburb

Not all Wellington suburbs perform the same from an investment perspective. One of the most common mistakes first-time investors make is assuming price growth alone guarantees a good outcome.

Understanding rental yield versus capital growth

Rental yield measures how much rent a property earns relative to its purchase price. Capital growth reflects long-term value increases.

For new investors, especially those buying a single property, yield often matters more in the early years. It helps cover mortgage costs and reduces financial pressure.

The QV House Price Index provides suburb-level insights into median values, historical growth, and market trends. Using this data allows investors to compare:

- Entry price by suburb

- Historical growth patterns

- Volatility during market downturns

Suburbs first-time Wellington investors often consider

While individual circumstances vary, many first-time Wellington property investors focus on areas with:

- Strong transport links

- Proximity to employment hubs

- Established rental demand

Suburbs such as Johnsonville, Newtown, Tawa, Kilbirnie, and parts of Lower Hutt often offer a balance between affordability and tenant demand. Central suburbs like Te Aro or Thorndon can deliver strong rents but usually come with higher purchase prices and lower yields.

Read our post and Explore the Rental Landscape in Wellington’s Suburbs.

Tenant demand indicators you should check

Experienced investors look beyond headline prices. Key indicators include:

- Vacancy rates

- Average days to rent

- Tenant demographics such as students, professionals, or families

- Proximity to hospitals, universities, and public transport

Property managers on the ground often have better insight into these factors than national reports alone. This is where professional advice becomes invaluable.

Financial preparation: Setting yourself up properly

Strong financial preparation is one of the biggest stress reducers for first-time investors.

Pre-approval and lending expectations

Most investors begin with a mortgage pre-approval. Lenders assess income, expenses, existing debt, and deposit size.

The Reserve Bank of New Zealand continues to influence lending conditions through interest rate settings and loan-to-value ratio rules. While policies can change, first-time investors should plan conservatively.

Typical considerations include:

- A larger deposit requirement for investment properties

- Higher interest rates than owner-occupied loans

- Stress testing repayments at higher rates

Budgeting beyond the purchase price

Buying a rental property in NZ involves more than just the deposit and mortgage.

First-time investors should budget for:

- Legal fees and conveyancing

- Building inspections

- Property management fees

- Insurance

- Rates and body corporate fees if applicable

- Initial maintenance or compliance upgrades

Many investors underestimate setup costs. A prudent buffer of several thousand dollars can prevent stress if unexpected repairs or vacancies occur early on.

The head versus heart approach: Why numbers matter more

One of the most important mindset shifts for a Wellington property investor is learning to separate emotion from analysis.

Why emotional buying creates risk

It is easy to fall in love with a property that looks appealing but performs poorly as a rental. Features that appeal to homeowners do not always matter to tenants.

Examples include:

- Expensive finishes that do not increase rent

- Layouts that reduce bedroom count

- Views that add cost but not yield

Successful investors focus on rental demand, compliance, and long-term resilience.

Key numbers every first-time investor should know

Before making an offer, you should understand:

- Expected weekly rent based on comparable listings

- Gross and net rental yield

- Ongoing expenses including management and maintenance

- Cash flow at current and higher interest rates

This data-driven approach removes much of the stress and uncertainty from the process.

Compliance and regulation: Planning ahead

Regulatory compliance is a reality of owning rental property in Wellington. Ignoring it creates financial and legal risk.

Healthy Homes Standards, insulation rules, and safety requirements should be factored into your purchase decision. Properties that are cheaper upfront may require significant upgrades before they can be legally rented.

Experienced property managers often conduct pre-purchase rental assessments to identify:

- Likely compliance costs

- Rental potential post-upgrade

- Risk areas such as moisture or heating

This is an area where first-time investors gain a real advantage by involving professionals early.

Next steps: Building the right professional team

Buying your first investment property without stress is rarely a solo effort.

Why a property manager matters from day one

Many first-time investors assume property management only becomes relevant after purchase. In reality, engaging a property manager early can influence better buying decisions.

A professional Wellington property manager can help with:

- Rental appraisals before purchase

- Understanding tenant demand by suburb

- Budgeting for realistic operating costs

- Compliance planning

- Reducing vacancy risk

This proactive approach often saves far more than it costs.

Other professionals you should involve

A strong investment team typically includes:

- A property-focused solicitor

- A mortgage adviser familiar with investment lending

- A building inspector experienced with Wellington housing stock

- A property manager with local market expertise

Working with professionals who understand property investment tips in NZ helps reduce surprises and build confidence.

Competitive insight: What most first-time investors are not told

Many guides focus only on buying. Experienced investors think beyond settlement day.

Key factors often overlooked include:

- How long a property will realistically remain rentable without major upgrades

- Whether the layout suits future tenant trends, such as remote work

- How well the property performs during vacancy periods

- Exit strategies if personal circumstances change

Stress usually comes from uncertainty. Planning for multiple scenarios is what separates confident investors from anxious ones.

Final thoughts: Investing with clarity and confidence

Your first investment property in Wellington does not need to be stressful. By focusing on research, conservative financial planning, objective decision-making, and professional support, you can enter the market with confidence.

At Taylor Property Plus, we work with first-time and experienced investors across Wellington to turn property ownership into a structured, manageable, and rewarding experience.

Frequently Asked Questions

Is Wellington a good place for first-time property investors?

Yes. Wellington offers strong rental demand, diverse tenant demographics, and long-term stability. However, suburb selection and compliance planning are critical.

How much deposit do I need for my first investment property?

Deposit requirements vary by lender and market conditions. Investment properties usually require a higher deposit than owner-occupied homes. A mortgage adviser can provide current guidance.

Should I use a property manager for my first rental?

For most first-time investors, yes. A professional property manager reduces risk, ensures compliance, and saves time and stress.

How do I estimate rental yield accurately?

Use comparable rental listings, local property manager appraisals, and suburb-level data from sources like the QV House Price Index.

What is the biggest mistake first-time investors make?

Buying emotionally instead of focusing on numbers. Successful investment decisions are driven by data, not personal taste.