Property portfolio diversification in Wellington refers to holding multiple property types, such as houses, apartments, and commercial units, to balance risk, income, and growth potential.

Diversifying a Wellington property portfolio means looking beyond standalone houses to include apartments, home-and-income properties, and selective commercial investments. A diversified strategy can improve rental yield, reduce risk, and future-proof returns. Success depends on suburb-level research, understanding risk tolerance, and working with experienced property management professionals.

Table of Contents

Introduction: Expanding Your Investment Horizons in a Dynamic Market

For many Wellington property investors, the journey begins with a single-family home. It is familiar, relatively straightforward, and historically reliable. However, as the Wellington property market matures and investor expectations shift, diversification is becoming less of a “nice to have” and more of a strategic necessity.

Rising interest rates, tighter lending conditions, and changing tenant demand mean that relying on one asset type can expose investors to unnecessary risk. Diversification allows Wellington property investors to balance cash flow, capital growth, and resilience across economic cycles.

For those building a long-term Wellington property investment strategy, the question is no longer whether to diversify, but how to do it wisely without adding stress or complexity.

Why Portfolio Diversification Matters in Wellington

How diversification looks across Wellington suburbs

Diversification is not just about adding new property types – it is also about understanding how different Wellington suburbs support different investment strategies. Rental yield, tenant demand, and asset suitability can vary significantly from one area to another.

The table below provides a suburb-level snapshot to help Wellington property investors identify where apartments, home and income properties, or selective commercial assets may fit into a diversified portfolio. It is designed as a strategic guide rather than a substitute for full due diligence.

Wellington Property Diversification and Yield Snapshot

| Suburb | Asset Types Best Suited | Typical Tenant Profile | Estimated Gross Yield Range | Strategic Insight |

| Te Aro | Apartments, mixed-use | Professionals, students | ~3.8% – 4.6% | Yield driven by density and demand; body corporate scrutiny essential |

| Newtown | Apartments, home and income | Hospital staff, families | ~4.2% – 5.0% | Balanced income and demand resilience |

| Karori | Houses, home and income | Families | ~3.6% – 4.3% | Lower yield; strong long-term tenancy stability |

| Johnsonville | Townhouses, duplexes | Families, commuters | ~4.5% – 5.3% | Transport access supports above-average yields |

| Lower Hutt (CBD fringe) | Apartments, small commercial | Professionals, SMEs | ~5.0% – 6.2% | Emerging diversification hotspot |

| Petone | Mixed residential-commercial | Retail tenants, renters | ~4.8% – 5.6% | Ideal for blended portfolios |

| Miramar | Houses, minor dwellings | Airport workers, families | ~4.1% – 4.9% | Stable demand with secondary dwelling upside |

| Thorndon | Apartments, executive rentals | Government professionals | ~3.7% – 4.4% | Income reliability over yield growth |

| Porirua | Duplexes, houses | Long-term renters | ~5.5% – 6.8% | Higher yields with higher tenant turnover risk |

Data note: Yield ranges below reflect typical gross rental yield bands based on aggregated insights from the Real Estate Institute of New Zealand (REINZ) and the QV House Price Index. Actual returns vary by property condition, financing, and management quality.

Diversification is a core principle of investing across all asset classes, and property is no exception. According to guidance from the Financial Markets Authority NZ, spreading investment risk across different asset types can reduce exposure to market volatility and unexpected downturns. You can explore their investor guidance through the Financial Markets Authority NZ website, which outlines best practices for long-term investment planning.

In Wellington specifically, diversification helps investors:

- Smooth cash flow during vacancy or maintenance cycles

- Reduce reliance on a single tenant demographic

- Capture multiple demand drivers across residential and commercial sectors

- Improve overall rental yield NZ-wide by balancing high-growth and high-income assets

Investing in Apartments: Pros and Cons in Wellington

Why Apartments Appeal to Wellington Investors

Apartment living has become increasingly attractive in Wellington, particularly in the CBD, Te Aro, Newtown, and near transport hubs. Demand is driven by students, professionals, and downsizers seeking convenience and affordability.

From an investment perspective, apartments often offer:

- Lower entry prices compared to standalone houses

- Strong rental demand in central locations

- Reduced external maintenance responsibilities

These factors can make apartments a practical diversification tool for investors seeking consistent occupancy.

The Challenges to Consider

However, apartments are not without complexity. Body corporate fees, long-term maintenance plans, and building quality are critical considerations. Investors must assess:

- Body corporate financial health

- Earthquake strengthening status

- Insurance coverage and levies

- Long-term maintenance schedules

Unlike standalone homes, these factors can materially impact net returns. Investors considering apartments should view them as income-focused assets rather than purely capital growth plays.

Home and Income Properties: Boosting Yield with Dual Streams

What Is a Home and Income Property?

A home and income property typically includes a primary dwelling plus a secondary self-contained unit, such as a granny flat or minor dwelling. In Wellington, this model is gaining traction due to housing density pressures and affordability constraints.

For investors focused on rental yield NZ, home and income properties can significantly enhance cash flow while spreading vacancy risk.

Yield and Risk Benefits

Key advantages include:

- Two income streams from one title

- Reduced vacancy impact if one unit becomes vacant

- Strong appeal to multi-generational tenants and professionals

In high-demand suburbs, well-designed secondary units can materially lift overall yield while maintaining strong tenant demand.

Regulatory Considerations

Investors should confirm compliance with local planning rules and building standards. Wellington City Council zoning rules can affect the legality and usability of secondary dwellings, making professional advice essential before purchase or development.

Commercial Property: Adding a New Dimension to Your Portfolio

Why Consider Commercial Property?

While often overlooked by residential-focused investors, selective commercial exposure can add stability and diversification. Commercial leases tend to be longer and may include tenant-paid outgoings, which can improve net returns.

Those exploring commercial property Wellington opportunities can find market insights through Wellington Commercial Property resources, which provide data on leasing trends, yields, and demand across retail, office, and mixed-use spaces.

Risks to Understand

Commercial property carries different risks than residential assets:

- Longer vacancy periods if a tenant leaves

- Higher upfront capital requirements

- Sensitivity to economic cycles and business confidence

For this reason, commercial assets are often best added once a residential base is well established.

What to Consider Before Diversifying

Risk Tolerance and Portfolio Balance

Every investor has a different comfort level with risk. Diversification should not mean complexity for its own sake. Instead, it should align with:

- Income needs versus growth objectives

- Time availability for oversight

- Financial buffers for unexpected costs

Educational resources like NZX’s Investor Education NZ provide useful frameworks for understanding risk profiles and long-term investment planning.

The Role of a Property Manager

As portfolios diversify, professional property management becomes increasingly valuable. A skilled Wellington property management team can:

- Manage multiple asset types efficiently

- Ensure compliance across residential and commercial properties

- Optimise rental pricing and tenant selection

- Reduce administrative burden and stress

This support allows investors to scale confidently while maintaining control and clarity.

Competitive Insight: What Many Investors Overlook

One of the most overlooked aspects of diversification is tenant segmentation. Many investors diversify asset types but fail to diversify tenant demographics. A balanced portfolio may include:

- Long-term family tenants

- Short-to-medium term professional renters

- Commercial tenants with stable lease structures

This layered approach can reduce correlated risk and stabilise income across market shifts.

Another often-missed factor is an exit strategy. Diversified portfolios provide more flexibility when selling or refinancing, allowing investors to adjust exposure without liquidating their entire position.

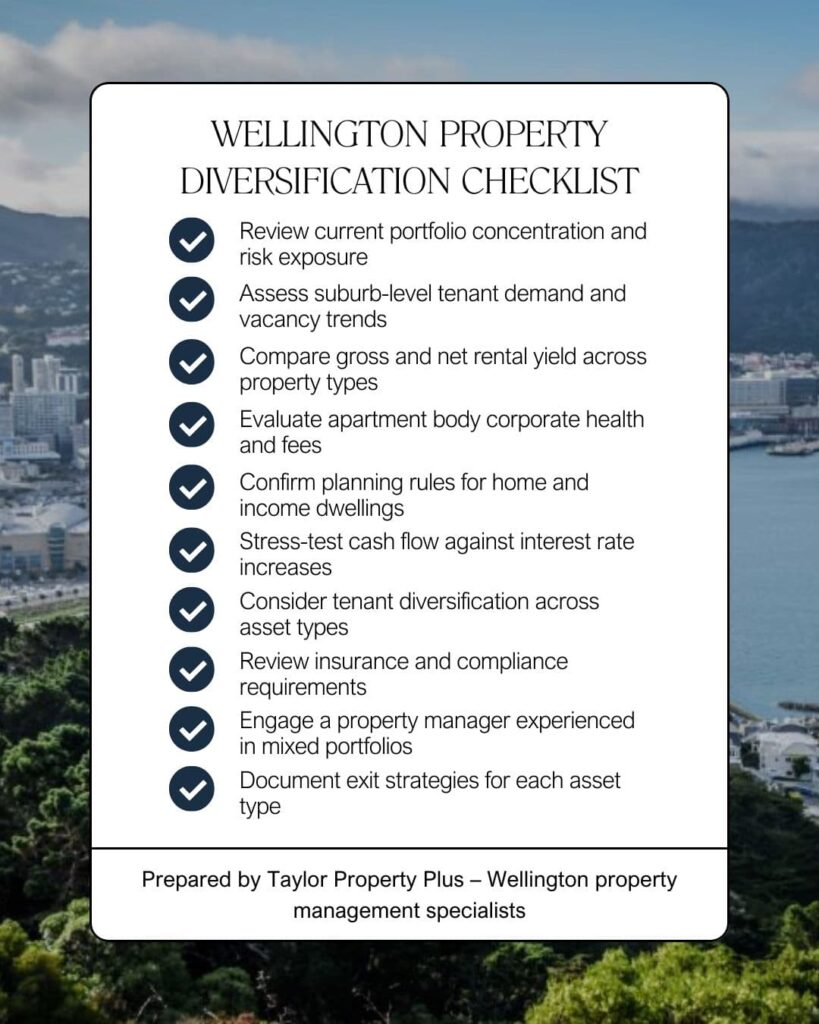

Final Thoughts: Building a Smarter Wellington Portfolio

Diversifying beyond the single-family home is not about abandoning what works. It is about building resilience, improving yield, and positioning yourself for long-term success in a changing Wellington market.

With careful research, realistic expectations, and the right professional support, diversification can transform a property portfolio from reactive to strategic.

At Taylor Property Plus, we work with first-time and experienced investors across Wellington to turn property ownership into a structured, manageable, and rewarding experience.

Frequently Asked Questions

What is property portfolio diversification in NZ?

Property portfolio diversification involves owning different types of property assets, such as houses, apartments, home and income properties, or commercial buildings, to spread risk and improve long-term returns.

Are apartments a good investment in Wellington?

Apartments can be a strong income-focused investment in Wellington, particularly in central locations. Investors should carefully assess body corporate costs, building quality, and long-term maintenance obligations.

What is a home and income property?

A home and income property includes a primary dwelling and a separate self-contained unit. This structure can increase rental yield and reduce vacancy risk.

Is commercial property suitable for residential investors?

Commercial property can complement a residential portfolio but carries different risks. It is generally better suited to investors with a stable residential base and sufficient financial buffers.

How can a property manager help with diversification?

A professional property manager can oversee different asset types, manage compliance, optimise rental income, and reduce administrative workload as portfolios grow.